Insurance is one of the most significant expenses for a pilot car driver, next to fuel and vehicle maintenance. Insurance rates have risen over the last two years, and one wonders why.

A CBIZ (a commercial insurance and financial services provider) article stated:

“…technological advancements have made vehicle repairs increasingly expensive. Combined with raised labor expenses and inflated vehicle prices, these issues have prolonged vehicle repair times and overall surging claim costs.”

CBIZ, along with others, is saying the sector is not profitable and, therefore, rates are increasing. AM-Best came out with a statistic that was more telling than anything else.

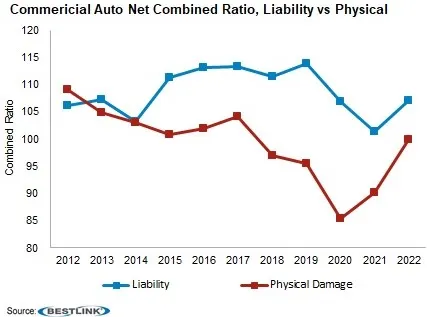

The above statistic shows the ratio of Liability damage, the blue line (damage to people), and Physical damage, the red line (damage to equipment, loads, cars, trucks).

It is telling that the red line has been steadily going down from 2012 to 2020 and increased markedly from 2020 to 2022. The blue line has been elevated but has not increased or decreased.

Also of note is that the red line dropped significantly in 2017. It was a time when the government reduced taxes and regulations across the boards, including for the fossil fuel sector. The government-induced lockdowns ended all that. A worldwide reduction in production and manufacturing caused huge backups. The lack of equipment, chips, and parts increased the prices of these items since they became very scarce, and some companies engaged in price gauging to take advantage of businesses that had to have the parts and chips and paid handsomely to obtain them to keep things going.

An active government-sponsored fossil fuel market suppression started in Spring 2020. If you suppress oil production, you will increase oil prices, and an increase in oil prices will raise the cost of all products that must be shipped from A to B by trucks. And that includes really everything. If you bought it, a truck brought it.

The WHY for the increase in insurance prices is government actions that resulted in supply distortions and inflation across many industries that recoiled on the insurance sector.

Florida

The state of Florida is on a war path when it comes to commercial auto insurance. The only one left in the state is Progressive, charging about $12,000 a year to cover a pilot car.

And why is that?

Per msn.com article of August 2023, 5 insurers are leaving Florida. The report covers mostly homeowner insurance companies and says Citizen Property Insurance Corp is now the most prominent company covering property insurance. The rest is going or already gone.

Per msn.com, it’s because of natural disasters, but this is BS. Florida has always had natural disasters since time immemorial!

In a July 2012 article, Newsweek reported, “On Tuesday, Farmers informed the state that it is discontinuing new coverage of auto, home and umbrella policies, a move that will reportedly affect 100,000 policies.” And most of them were commercial policies.

Newsweek says Florida’s legislature has tackled the issue recently. Still, much of the focus has been on shielding insurance companies from lawsuits and setting aside money for re-insurance to help protect insurers.

And that is a wrong target.

What seems to be more of a problem is a state plagued by massive price gauging in the real estate sector and the automobile market, plus lots of insurance fraud.

And then there was Senate Bill 54…

The state had a no-fault personal injury protection (PIP) system, and the bill intended to change this to a mandatory $25,000 bodily injury coverage.

PIP coverage is complex. You buy it as part of the insurance you purchase on your car, but it covers you in situations even when you’re not in that car. It also sometimes covers your relatives, if they live with you, or your passengers.

If it is complicated, it can be tampered with. And fraudulent claims are high.

The $10,000 PIP coverage amount was set in the 1970s. The $10,000 doesn’t go nearly as far now as in the seventies. It also means it can’t be the sole cause of high rates. But it may be the sole cause of fraudulent claims.

One thing is sure. No-fault states have higher insurance rates than states that don’t have it. Again, I was unable to determine if fraudulent claims were the sole source. The $10,000 limit isn’t a big deal since most accidents have much higher settlements, even in non-no-fault states.

Much of the focus by Florida politicians has been on shielding insurance companies from lawsuits and setting aside money for re-insurance (insurance for insurance firms) to help protect insurers.

Per Carey, Leisure & Neil, a law firm in Clearwater, Florida, “Governor Ron DeSantis vetoed the bill when it was proposed, alleging it may drive insurance costs up for Florida residents. He claimed that this could result in more uninsured drivers on the road. He also feared that the change would expose insurance companies to more “bad-faith” litigation in the future.”

Notice DeSantis says it could result in higher rates, but will it do that? Where is the investigation, data, facts? It is typical for politicians who guess and don’t do their homework.

It is unclear where this is going right now.

There is just one thing for sure: No-fault states have higher rates. No-fault states also have higher fraudulent claims.

So what will you do about it, DeSantis et al.?

You better act fast. You may wake up one day and find no commercial auto insurance available anymore in Florida.